The Federal Reserves Current Framework for Monetary Policy a Review and Assessment

Monetary Policy Objectives

Bank Republic of indonesia is mandated with creating and maintaining rupiah stability. That mandate is explicitly stipulated in Act No. 23 of 1999 concerning Bank Indonesia, as amended by Act No. 3 of 2004 and Human action No. vi of 2009 in Article vii. Rupiah stability encompasses two dimensions. Outset, rupiah stability is the toll stability of goods and services, as reflected by inflation. The second dimension relates to rupiah exchange rate stability against other currencies. Indonesia implements a complimentary-floating exchange rate regime and exchange rate stability is necessary to achieve and maintain cost and financial system stability.

In pursuit of its mandate, Bank Indonesia adopted the Inflation Targeting Framework (ITF) as its budgetary policy framework on 1st July 2005. ITF is relevant for the mandate and institutional arrangements mandated in prevailing laws. Based on ITF, inflation is the overriding objective. Notwithstanding, Banking company Indonesia continues to refine its monetary policy framework based on the changing dynamics and economic challenges faced in gild to increase effectiveness.

Monetary Policy Framework

In the implementation of budgetary policy, Banking concern Indonesia applies an Aggrandizement Targeting Framework (ITF). ITF is a framework of publicly announcing an inflation target corridor and adjusting monetary policy to achieve that target equally part of the delivery and accountability of the fundamental banking company. In practice, ITF is implemented using a policy rate as a point of monetary policy and the interbank rate as the operational target. The Aggrandizement Targeting Framework was formally adopted by Bank Republic of indonesia on 1st July 2005, replacing base money every bit the target of monetary policy.

Based on experience from the Global Financial Crisis in 2008/2009, an of import lesson that emerged was the need for adequate central bank flexibility in response to more complex economical developments and a stronger fiscal sector influence on macroeconomic stability. Consequently, Bank Indonesia strengthened the ITF framework through its evolution into Flexible ITF.

What is Flexible ITF?

Flexible ITF was adult effectually the core elements of the existing Inflation Targeting Framework (ITF), including a publicly announced inflation target and forwards-looking monetary policy, namely monetary policy oriented towards achieving the aggrandizement target in time to come periods due to the time lag effect of monetary policy.

Public accountability of monetary policy remains an inherent element of Flexible ITF. Flexible ITF was developed based on the post-obit 5 core elements:

- Inflation targeting as the central strategy of budgetary policy.

- Integration of monetary and macroprudential policies to strengthen policy transmission and maintain macroeconomic stability.

- The role of exchange charge per unit and capital letter flow policies to support macroeconomic stability.

- Strengthening policy coordination between Banking company Indonesia and the Authorities to control inflation too as maintain budgetary and fiscal system stability.

- Strengthening the policy advice strategy as a policy instrument.

Why Flexible ITF?

The Global Financial Crisis that occurred in 2008-2009 forced central banks to rescue the economy and maintain fiscal system stability. Furthermore, policies that focused solely on ITF implementation were no longer considered sufficient due to the narrow monetary policy mandate of maintaining aggrandizement in line with the target corridor, which was bereft to maintain overall economic organisation stability.

The role of the fiscal system in the economic system is increasing, with the impact of financial system instability becoming more meaning. This is reflected in the massive recovery costs and far-reaching impact of the Global Financial Crunch in 2008/2009. Such conditions raised sensation of the critical central bank function to maintain financial organisation stability. Consequently, ITF implementation to maintain price stability was necessary simply not sufficient.

After the Global Financial Crisis, however, growing need emerged for cardinal banks to strengthen financial system stability in guild to ensure macroeconomic and financial sector stability. To that stop, successful ITF implementation required support of a macroprudential regulatory framework. Therefore, Bank Indonesia evolved ITF into Flexible ITF by strengthening its mandate to maintain price stability and back up financial system stability.

How is Flexible ITF Practical?

The overriding objective of ITF and Flexible ITF are the same, namely to control inflation. Notwithstanding, a nascent dimension that emerged from the Global Financial Crisis was the central depository financial institution's integrated office to maintain financial system stability, while achieving the price stability mandate. The embodiment of Flexible ITF is the flexibility to integrate monetary and financial system stability through a policy mix of budgetary, macroprudential, exchange charge per unit and upper-case letter flow instruments, while strengthening the institutional arrangements in order to optimise the part of policy coordination and advice.

In accord with the inflation targeting strategy, Depository financial institution Republic of indonesia announces the aggrandizement target for a specific future period. The inflation target is set up by the Government in coordination with Depository financial institution Republic of indonesia for the upcoming three years through a Minister of Finance Regulation (PMK). Banking company Republic of indonesia regularly evaluates whether the inflation projections remain in line with the target corridor fix. The projections are based on several models and the various data bachelor that depict inflation conditions moving forwards as the ground for the monetary policies instituted. This is due to the implications of the time lag effect of monetary policy, with the monetary policy target thus based on futurity inflation projections. Efforts to achieve the target are implemented through a policy mix response based on transparency and accountability.

Bank Republic of indonesia regularly reports the implementation of its duties to the People'south Representative Council (DPR) and likewise the Government. Furthermore, Bank Indonesia also routinely publishes assessments of the latest inflation conditions and outlook moving forward, the decisions taken as well as future policy direction to maintain inflation in line with the target (frontward guidance). This is not only done under the auspices of transparency, yet also an important aspect of strengthening Bank Indonesia credibility to ensure policy effectiveness.

To strengthen the effectiveness of monetary policy transmission, Bank Indonesia set the BI 7-Day (Opposite) Repo Rate as the policy rate on 19th August 2016, representing the monetary policy response signal in terms of controlling inflation in line with the target corridor. Use of BI7DRR as the reference rate is function of Bank Indonesia's monetary policy reformulation.

Previously, Banking company Indonesia had used the BI Rate every bit the reference rate, equivalent to a 12-calendar month interest rate in the term structure of monetary operations. Through the BI7DRR, still, the tenor of the monetary instrument was shortened to vii days, which is expected to accelerate monetary policy transmission and steer inflation towards the target corridor.

There were three main objectives of monetary policy reformulation. Starting time, strengthening the signal of monetary policy management. 2nd, strengthening monetary policy manual effectiveness through its touch on involvement rate movements in the money marketplace and banking industry. Third, accelerating financial marketplace deepening, particularly in terms of transactions and germination of the interest charge per unit construction in the interbank money marketplace for tenors of 3-12 months.

In practice, budgetary policy reformulation upholds four salient principles. First, reformulation does not change the monetary policy framework as Banking company Indonesia continues to utilise flexible ITF. Second, reformulation does not change the electric current budgetary policy stance. Third, reformulation ensures the policy rate is reflected in monetary instruments and is transactable with Depository financial institution Indonesia. Fourth, determination of the operational target based on diverse considerations can be influenced by the policy rate. Consistent with the second principle, reformulation does non change the current monetary policy opinion considering both the BI Rate and BI7DRR are part of the same term structure with regards to guiding inflation towards the respective target.

The implementation of Flexible ITF also aims to attain financial system stability. To that end, Flexible ITF implementation is supported past the application of macroprudential policy. Macroprudential policy focuses on the interactions betwixt financial institutions, markets, infrastructures and the broader economy, including measurement of time to come potential risk. Such policy aims to foreclose systemic risk that could trigger a financial system crisis due to macroeconomic atmospheric condition. An in-depth explanation of macroprudential policy is available at the following link: (Link ke kebijakan makroprudensial).

Flexible ITF implementation is likewise supported by exchange charge per unit policy. Bank Indonesia institutes substitution rate policy in order to manage rupiah commutation rates in line with the currency's fundamental value and marketplace mechanisms. Furthermore, exchange rate policy aims to reduce shocks that sally from a demand and supply mismatch in the foreign substitution market through selling intervention in the spot market, Domestic Not-Deliverable Forwards (DNDF) market an FX futures market likewise as through purchases of tradeable government securities (SBN) in the secondary marketplace. This strategy simultaneously maintains substitution rate stability an adequate rupiah liquidity.

The various aforementioned policies are strengthened through policy coordination with the Government, especially on the supply side. Government policy is predominantly oriented towards maintaining affordable prices, uninterrupted supply and distribution as well every bit effective communication in order to stabilise food prices and control inflation. Policy coordination between Bank Republic of indonesia and the Authorities to command inflation has been strengthened through the establishment of a National and Regional Aggrandizement Task Forces (TPI). In addition, policy coordination also reinforces financial system stability. Through the Financial System Stability Commission, Bank Indonesia in conjunction with the Ministry of Finance, Indonesian Financial Services Authority (OJK) and Deposit Insurance Corporation (LPS) determine which coordination measures are necessary and provide recommendations in terms of monitoring and maintaining fiscal organisation stability.

The overriding objective of monetary policy is to create and maintain rupiah stability, as reflected by low and stable inflation. To that finish, Depository financial institution Indonesia sets the BI seven-24-hour interval (Reverse) Repo Charge per unit as the principal policy instrument that influences economic activeness, with inflation as the ultimate goal. The process of setting the BI7DRR to achieving the inflation target is transmitted through diverse channels with a time lag.

Adjusting the BI7DRR to influence inflation is known as the monetary policy transmission machinery. This mechanism shows how Bank Indonesia policy, through adjustments to monetary instruments and the operational target, influences various economical and financial variables before ultimately affecting inflation. The machinery works through interactions between the fundamental bank, banking industry and financial sector, as well as the existent sector. Adjustments to the BI7DRR influence inflation through diverse channels, including the interest charge per unit channel, credit channel, exchange rate channel, asset price channel and expectations channel..

In terms of the interest rate aqueduct, adjustments to the BI7DRR influence deposit rates and lending rates in the banking industry. Depository financial institution Indonesia tin apply tight-bias monetary policy by raising interest rates, which impacts aggregate need and alleviates inflationary pressures. In contrast, reducing the BI7DRR will lower lending rates thus increasing corporate and household demand for loans. In add-on, lower lending rates also reduce the cost of majuscule for investment in the corporate sector, thus stoking consumption and investment activeness and stimulating the economy..

Adjustments to the BI7DRR tin also influence the exchange rate through the exchange rate channel. A hike in the BI7DRR, for example, would increase the differential betwixt interest rates in Republic of indonesia and other countries. A wider interest charge per unit differential would attract non-resident investors to place capital in financial instruments in Indonesia seeking a higher rate of render. In plough, the foreign capital arrival would trigger rupiah appreciation, leading to cheaper imports and more expensive, or less competitive, exports from Indonesia, thus stimulating higher imports while simultaneously reducing exports. Consequently, rupiah appreciation would ease inflationary pressures.

The touch on of changes in involvement rates on economical activity also influences public inflation expectations through the expectations channel. Lower interest rates stimulate economic activeness an increase inflation, with workers thus anticipating higher inflation and, hence, demanding higher wages. Producers subsequently pass on the price of college wages to consumers by raising prices.

The monetary policy transmission machinery is characterised by a variable time lag. The time lag associated with each manual channel is different. Nether normal conditions, the cyberbanking industry will respond to increases/decreases in the BI7DRR by raising/lowering interest rates. Withal, if the banking industry detects higher risk in the economy, the response to a downward BI7DRR movement is slower. In addition, in the case of cyberbanking industry consolidation to increase capital, lower lending rates and increasing demand for loans do not necessarily increase banking concern lending in response. On the demand side, consumers may non necessarily answer to lower lending rates in the cyberbanking industry through higher demand for loans if the economic outlook is weak. Therefore, the effectiveness of monetary policy transmission is affected by external conditions, the financial sector and banking manufacture, equally well as the existent sector.

Transparency and Communication

In accordance with Act No. 23 of 1999 concerning Banking concern Indonesia, as amended by Deed No. 3 of 2004 and Deed No. 6 of 2009, Article 4, Paragraph 2 states that Banking concern Indonesia is an contained institution, free from government and third-party interference, unless explicitly stipulated in prevailing laws and regulations. Institutional independence is balanced against transparency and accountability.

Transparency

The principles underlying monetary policy transparency ensure that the information communicated allows the public to empathise and anticipate the decisions taken past the central bank to achieve the overriding objective. Therefore, the purview of data communicated to the public is equally follows:

- Objective

The primal bank explicitly and consistently communicates what is to exist accomplished by monetary policy in terms of the overriding and brusk-term objectives, as well as the rationale behind those objectives. - Method

Central bank transparency in relation to procedural activities in budgetary policy, including communicating the monetary operations undertaken, the results of economical modelling and projections as well every bit the basic assumptions used, in order to course expectations in the financial markets as well equally prevent and minimise market place shocks. In add-on, this is required to raise public understanding of the central bank'southward monetary policy. - Decision Making

The central banking company announces the policies taken forth with the underlying considerations, such equally a conclusion to raise the policy charge per unit, immediately after the decision has been made.

In addition, the scope of transparency in budgetary policy is also contained inside the "Lawmaking of Proficient Practices on Transparency in Monetary and Fiscal Policies", which has been developed by the International Monetary Fund (Imf) since 1999 and is currently applied by many of its members. The Code contains a number of key proficient practices equally follows:

- Clarity of roles, responsibilities and objectives of the monetary policy dominance;

- Open process for formulating and reporting monetary policy decisions;

- Public availability of information on monetary policy; and

- Accountability and assurances of integrity by the monetary authorisation.

Monetary Policy Communication

Monetary policy effectiveness tin can be improved through effective communication, especially during periods of heightened uncertainty. As the monetary potency, Depository financial institution Republic of indonesia only has direct influence over brusque-term interest rates, while long-term interest rates are determined more than by futurity expectations of budgetary policy, which can be directed through policy communication.

Advice contributes to stronger transparency and accountability at Bank Indonesia by providing greater public understanding in terms of monetary policy in general, while forming public and market place expectations as well as reducing future dubiety. Banking concern Indonesia conducts monetary policy communication through various media every bit follows:

- Press Releases and Press Conferences;

- Publications, including the Monetary Policy Written report, Monetary Policy Review, Economic Report on Republic of indonesia, Quarterly DPR Study and and then on;

- Bank Indonesia website too as various digital and social media platforms;

- Talk shows aired on radio and telly;

- Seminars and discussions with stakeholders; and

- Regional broadcasting.

Accountability

Deed No. 23 of 1999 concerning Depository financial institution Indonesia, as amended by Act No. 3 of 2004 (equally amended by Act No. half-dozen of 2009), mandates accountability at Bank Indonesia in the implementation of duties, responsibilities and budget.

PThe principles of accountability in terms of implementing Banking company Indonesia's duties and responsibilities are applied through the directly public communication of information via the mass media at the get-go of each year apropos an evaluation of monetary policy implementation in the previous year likewise as the monetary policy direction and targets for the upcoming year. Furthermore, such information is besides communicated in writing to the President and People'southward Representative Quango (DPR) of the Commonwealth of Indonesia.

Accountability also closely relates to independence. More than independence enjoyed by a central bank demands greater accountability.

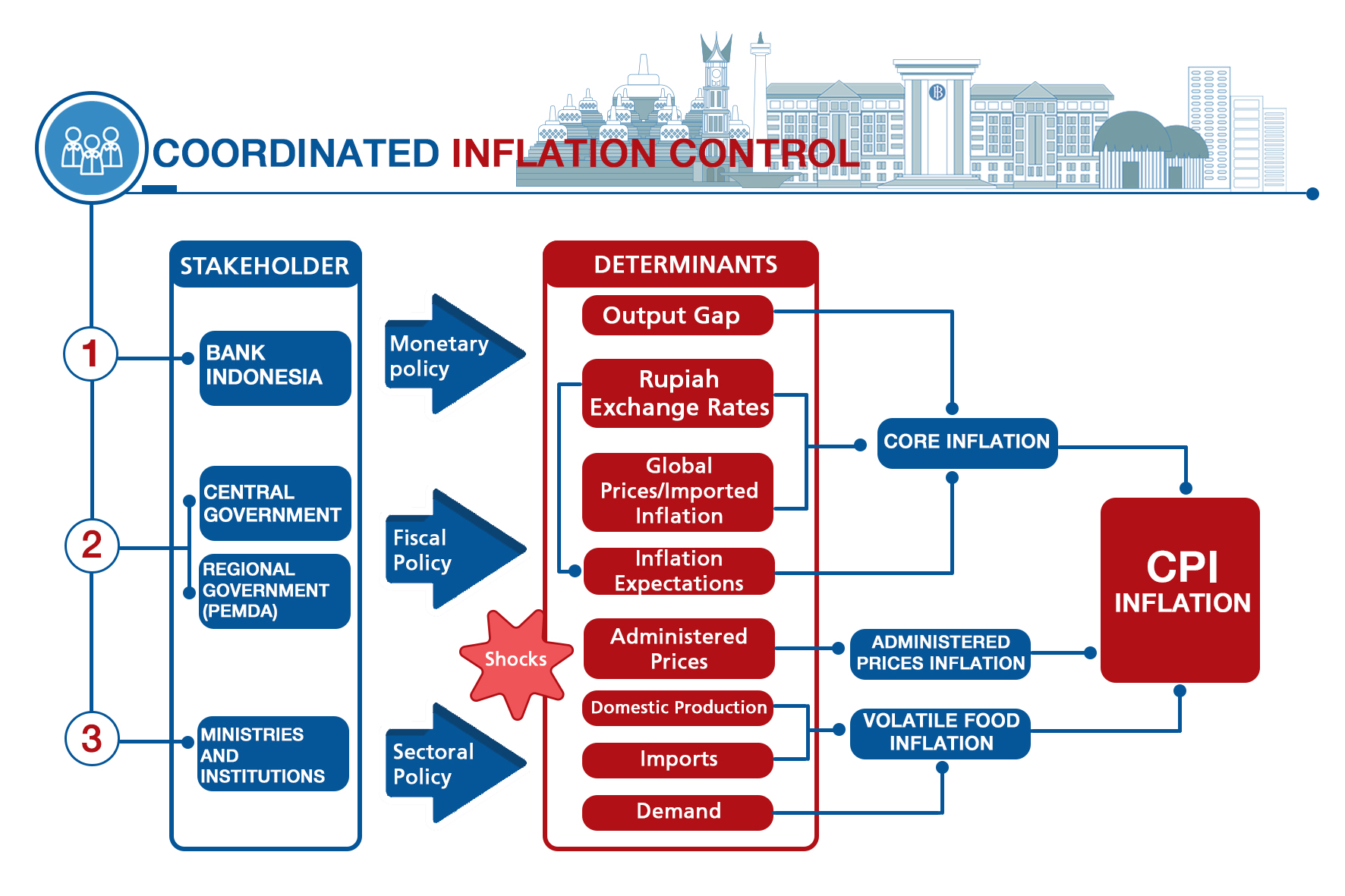

Low and stable aggrandizement are prerequisites for public prosperity in line with the macro policy goals. Withal, sources of inflationary pressures not only originate from the need side, which can exist managed by Bank Republic of indonesia, but also stalk from the supply side in relation to the production and distribution of appurtenances. In add-on, inflation shocks may also emerge due to government policy concerning administered prices, such as fuel and other energy prices. Therefore, a policy mix is required in order to achieve low and stable inflation.

Bank Republic of indonesia coordinates with the fundamental and local government to control aggrandizement. Meanwhile, the Government also plays a role in terms of controlling inflation expectations and managing supply through the management of supply, distribution, connectivity, merchandise chain and subsidies. Synergy is formed to control aggrandizement within the predetermined target corridor through the establishment of aggrandizement task forces. A central aggrandizement job force (TPI) was established in 2005, with regional inflation chore forces later on formed since 2008.

Coordinated inflation control was strengthened through Presidential Regulation (Perpres) No. 23 of 2017 concerning the National Inflation Job Force (TPIN) as a legal foundation. The Presidential Regulation stipulated the coordination mechanism for aggrandizement control through the formation of a Central Aggrandizement Task Forcefulness (TPIP), as well as Regional Aggrandizement Job Forces (TPID) at the provincial and city/regency level.

The legal foundation was subsequently bolstered by a promulgation of Coordinating Minister of Finance Regulation No. 10 of 2017 concerning the Mechanisms and Procedures for TPIP, Provincial TPID and City/Regency TPID, Analogous Minister of Finance Regulation No. 148 of 2017 concerning the Duties and Membership of Working Groups and TPIP Secretariat, and Government minister of Dwelling Affairs Prescript No. 500.05-8135 of 2017 concerning the Regional Inflation Task Forces (TPID). The inflation control plan focuses on 4K principles as follows:

- Affordable prices.

- Available supply.

- Uninterrupted distribution.

- Constructive communication.

Source: https://www.bi.go.id/en/fungsi-utama/moneter/default.aspx

0 Response to "The Federal Reserves Current Framework for Monetary Policy a Review and Assessment"

Postar um comentário